In 2017 alone, smartphone suppliers shipped some 1.5 billion devices to end users worldwide, accounting for $479 billion in global sales.1,2

Combined figures for 2010–2020 indicate that total global smartphone shipments are expected to surpass 13 billion devices—almost two smartphones for every person currently inhabiting the planet.3

That is a lot of phones—and a remarkable number when you consider the relative obscurity of smartphones only about a decade ago.

“The past 10 years have witnessed a revolution in mobile communication that has swept us from the cellphone era into the amazing smartphone age,” Kyocera spokesperson Jay Scovie says in an interview. “But without advanced ceramics and high-tech glass, this revolution would never have happened.”

Dialing in: State of the global smartphone market

Although IBM released the first smartphone back in 1994, the market remained relatively niche until Apple released the iPhone in 2007. Since that time, the market has exploded.

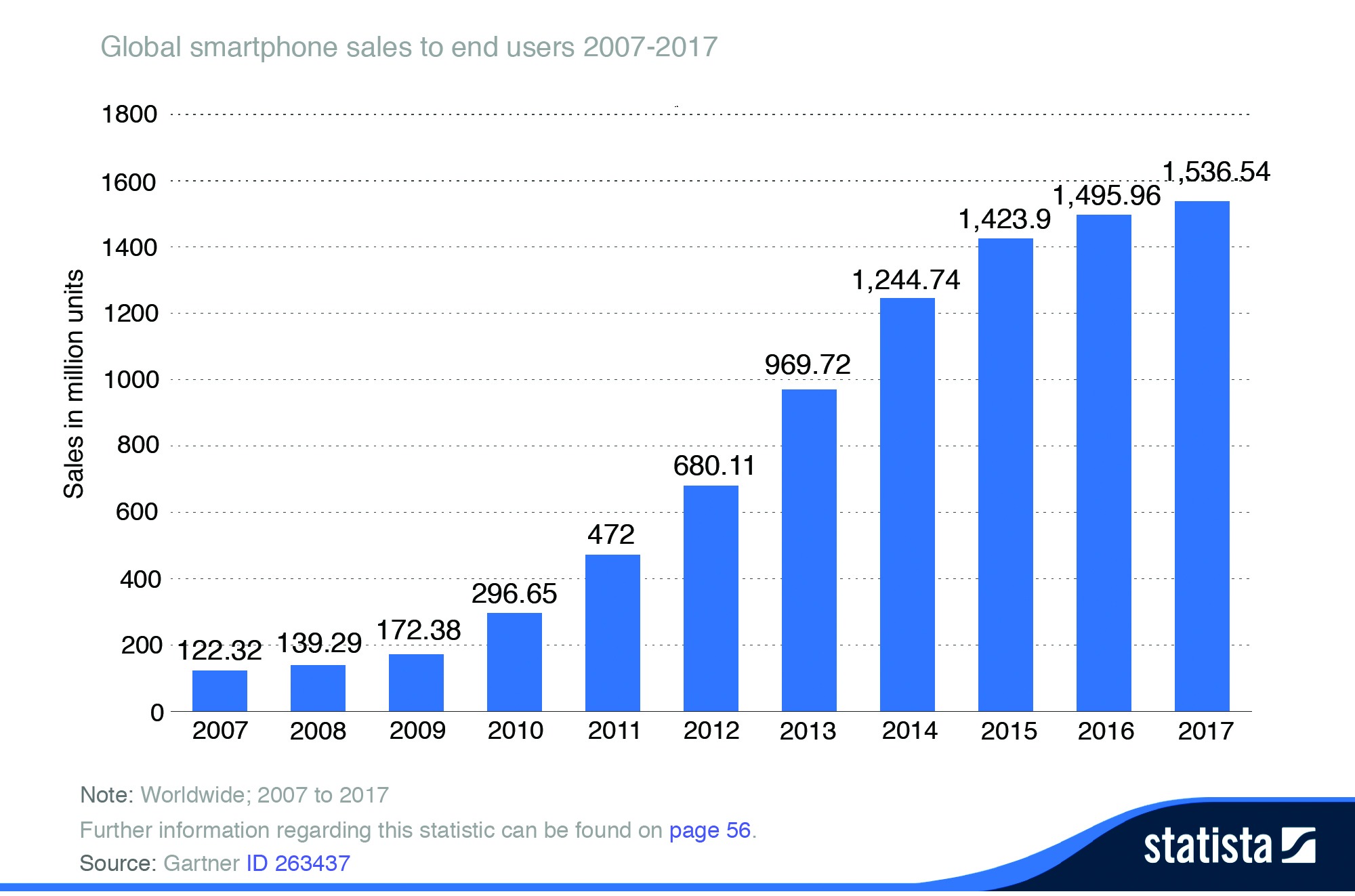

While around 122 million smartphones were sold worldwide in 2007, that number reached more than 1.5 billion by 2017.1

In 2011, only about 10 percent of the total global population used a smartphone. Today, there are an estimated 2.5 billion smartphone users worldwide, roughly a third of the planet’s inhabitants.4 Narrow the focus to developed or developing countries, and about 80 percent of people own a smartphone.5 And by 2025, estimates predict there will be 5.9 billion unique mobile subscribers, or 71 percent of the entire global population.6

Initial smartphones were primarily designed to call, message, and email—functions with a business focus. But Apple gave the world a bite of something different with the iPhone, introducing the world to a thin, sleek, multimedia experience for the everyday user.

Fast forward to today, and it is easier to think about what smartphones cannot do rather than list the things they can do. It is this multifunctionality that partially accounts for the smartphone’s electric rise in the consumer electronics world and in our daily lives.

Figure 1. Number of smartphones sold to end users worldwide from 2007 to 2017 (in million units).

Smartphones shipments are estimated to grow at a compound annual growth rate (CAGR) of 2.8 percent to reach 1.68 billion units by 2022.7 Global smartphone sales are estimated to generate revenues of almost $479 billion in 2017, an approximate 45 percent increase from 2013 figures.2 Revenues are expected to continue growing at a CAGR of 19.0 percent to reach a value of more than $1.5 trillion by 2026, indicating much gain for those in the smartphone market8 (Figures 1, 2).

Figure 2. Smartphone sales value worldwide from 2013 to 2017 (in billion U.S. dollars), by region.

Gains are estimated to stretch beyond the direct industry as well. The mobile ecosystem is estimated to have directly and indirectly supported some 29 million jobs in 2017.6 And the mobile industry contributes some $3.6 trillion to global gross domestic product (4.5 percent), a number that is predicted to rise to $4.6 trillion (5.0 percent) by 2022.

Geographically (Figure 3), the main players in the smartphone market are no surprise—China leads, with $152 billion of smartphone sales value in 2017, almost a third of the market. North America trails behind with $84 billion in sales value in the same time, most of those sales coming from the United States.9

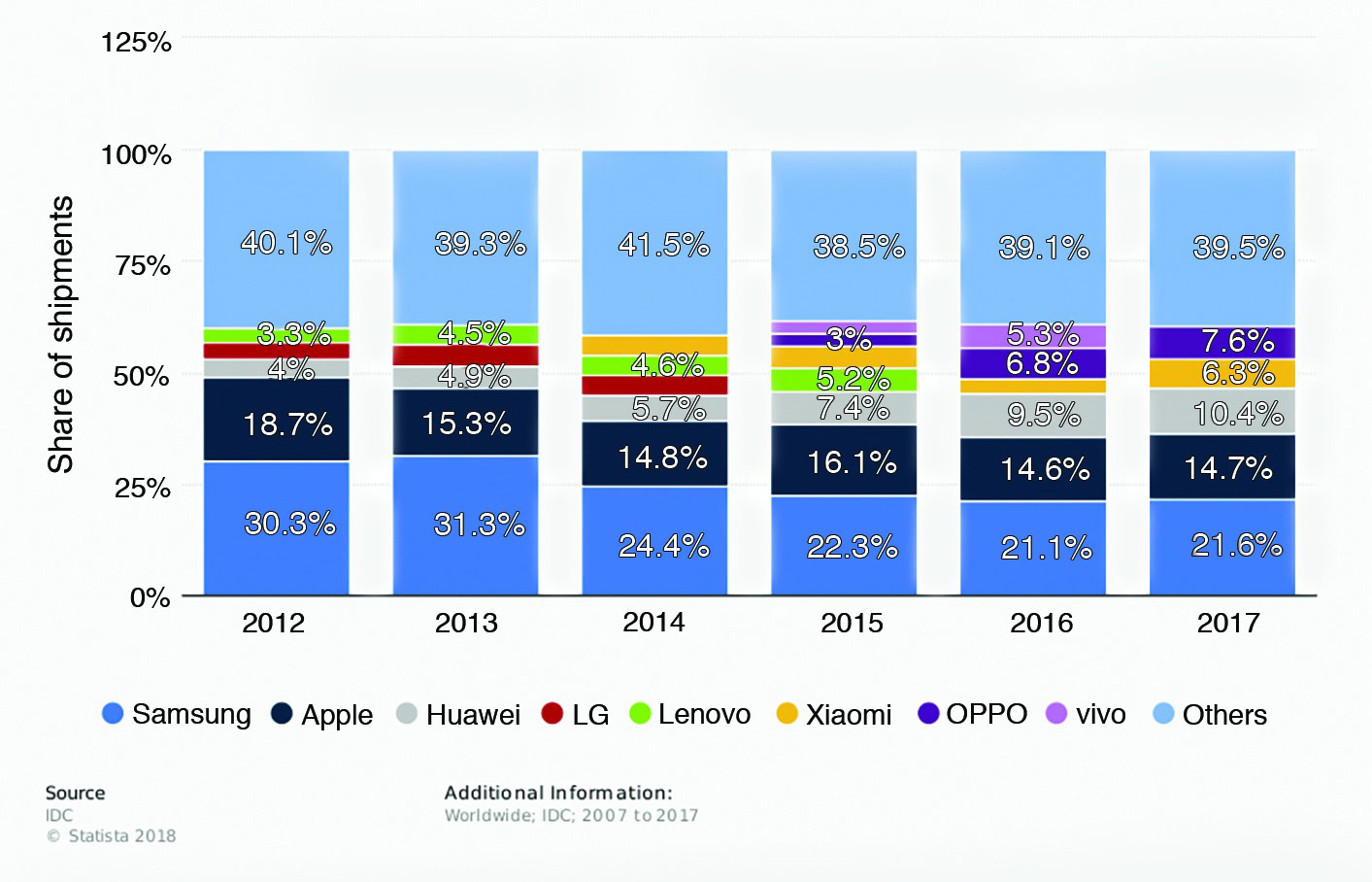

Figure 3. Share of smartphone shipments worldwide from 2012 to 2017 by vendor.

These markets represent significant portions of individual economies. According to the International Monetary Fund, China exported $107 billion worth of smartphones in 2016, an amount that totals 5 percent of the country’s total exports.10 As a main supplier of smartphone components, South Korea’s semiconductor exports comprised a whopping 17 percent of its total exports in 2016.

Similarly, top smartphone suppliers hail from China, South Korea, and the U.S. Of the top 12 smartphone suppliers, nine are headquartered in China, two in South Korea (Samsung and LG), and one in the U.S. (Apple).

Samsung, the reigning champion smartphone supplier, accounted for 21.6 percent of global smartphone shipments in 2017, with Apple securing the silver spot with 14.7 percent of total shipments.11 Chinese manufacturers follow, with Huawei, OPPO, and Xiaomi each clenching 6–10 percent of the market (these brands are delivering some of the highest growth rates).

In terms of smartphone revenue, however, Apple has the top spot, with 2018 reports indicating the company controls 51 percent of the global smartphone revenue share (partially due to release of its high-end iPhone X model), while Samsung holds only 15.7 percent.12

Beyond the major end-device suppliers, it takes an entire supply and manufacturing chain to build a smartphone. From the raw materials that supply component manufacturers to the semiconductor industry, the smartphone industry stretches far and wide.

Background image credit: iStock.com/Nastco

Dialing out: What next?

In general, the past few years have averaged minor annual increases, on the order of a few percent, in the global smartphone market. Compared to the market’s exponential growth in the early 2010s, when CAGRs exceeded 50 percent, these new figures indicate much more modest growth and potentially leveling of the market.7

The second quarter of 2018 noted a 1.8 percent decline in smartphone unit shipments year over year, although quarterly figures tend to fluctuate with the timed release of certain manufacturers’ new device models. Nonetheless, some analysts predict these figures indicate stalling of the market.13

With market saturation approaching 80 percent in developed countries, that may not be surprising. Future growth in the smartphone market is predicted to be driven by developing countries, including India, China, Pakistan, Indonesia, and Bangladesh.6

While fewer than 25 percent of Americans keep their smartphones beyond the two-year mark—43 percent opt to replace their devices every year14—those figures may significantly change as the market for high-end devices continues to rise. With some new smartphone models costing upwards of $1,000, users may replace their devices less often, creating further competition for suppliers.

Over the past few years, smartphones have seen relatively minor incremental changes and upgrades. The International Monetary Fund estimates that the new tech cycle peaked in 2015, with declines in the smartphone market in China first noted in 2017.10

However, the increasingly competitive climate is spurring suppliers to push innovation further, incorporating enhanced technologies in an effort to sell the latest device models.

“To keep up with the increasing demand for the new artificial intelligence, augmented reality/virtual reality, contextually aware, and 5G functionalities headed to the market, we expect growth to come from improvements in overall core functions in the near term,” says Anthony Scarsella, research manager with the International Data Corporation’s Worldwide Quarterly Mobile Phone Tracker, in a March 2018 market forecast.15 “Improvements in speed, power, battery life, and general performance will be critical in driving growth at a worldwide level as the smartphone evolves into a true all-in-one tool.”

Even with the current slowed growth, the size of the smartphone industry is massive, which means huge potential, profit, and opportunity for the diverse markets that support, supply, and are otherwise connected to the global smartphone consumption.

Enabled by ceramics and glass

“In the era of the smartphone, there are a surprising number of ceramic components within an average mobile device, including capacitors, filters, antennas, and substrates for image sensors,” wrote Arne Knudsen in a 2018 ACerS Bulletin article. “With the sale of mobile phones approaching nearly two billion units annually, the number of ceramic components in phones is at least an order of magnitude higher.”16

Nearly everywhere you look within a smartphone—whether an end component itself, the component’s individual parts, or the manufacturing or processing steps that enabled that component—you can find ceramic and glass materials at some step along the way. Some are immediately recognizable, like the contribution of ceramics in the microcrystal zirconium oxide outer back casing of the Xiaomi Mi Mix 2 or the all-ceramic back of Essential brand’s smartphone model, simply called Phone. The contribution of Corning’s Gorilla Glass to cover screens is also clear in the approximate six billion devices that incorporate the ion-strengthened glass. Some ceramic components, however, are hidden well beyond the scenes.

“A few years ago, you would have needed a dozen individual devices to do all the things you can do with a single smartphone today. Ceramic-based components and high-tech glass deserve much of the credit,” says Scovie.

Figure 4. Ceramics and glasses serve multiple functions in smartphones: structural, display, electronics, and sensors. Background credit: iStock.com/adventtr

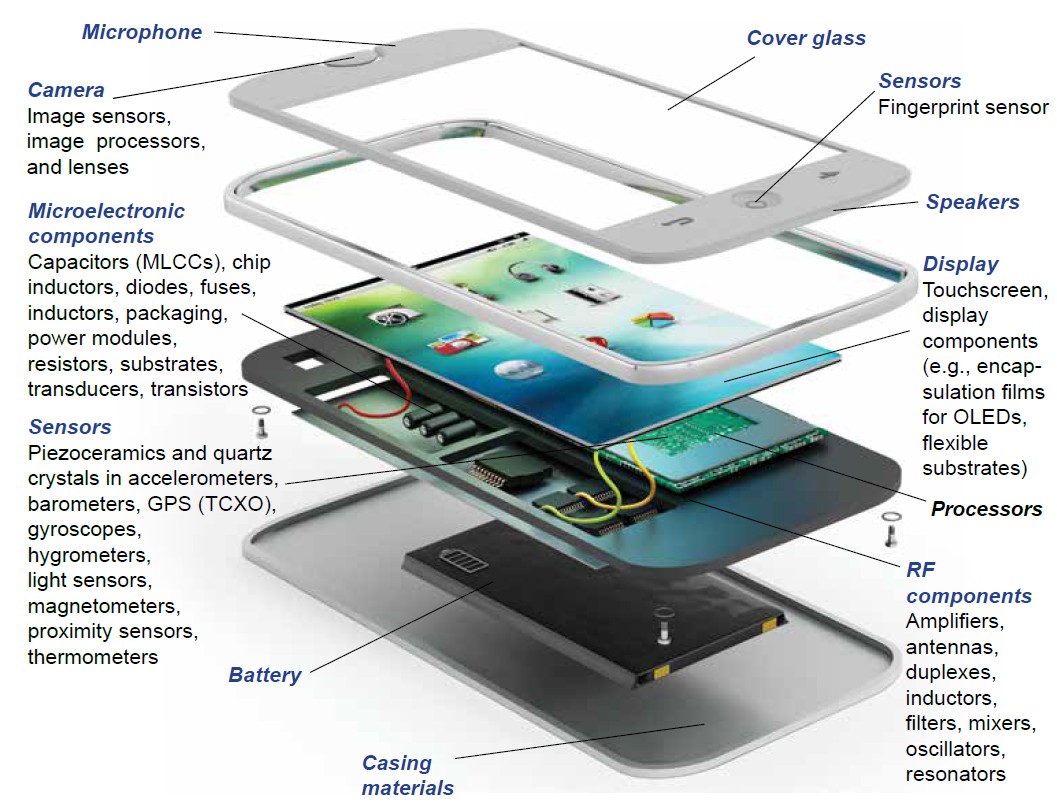

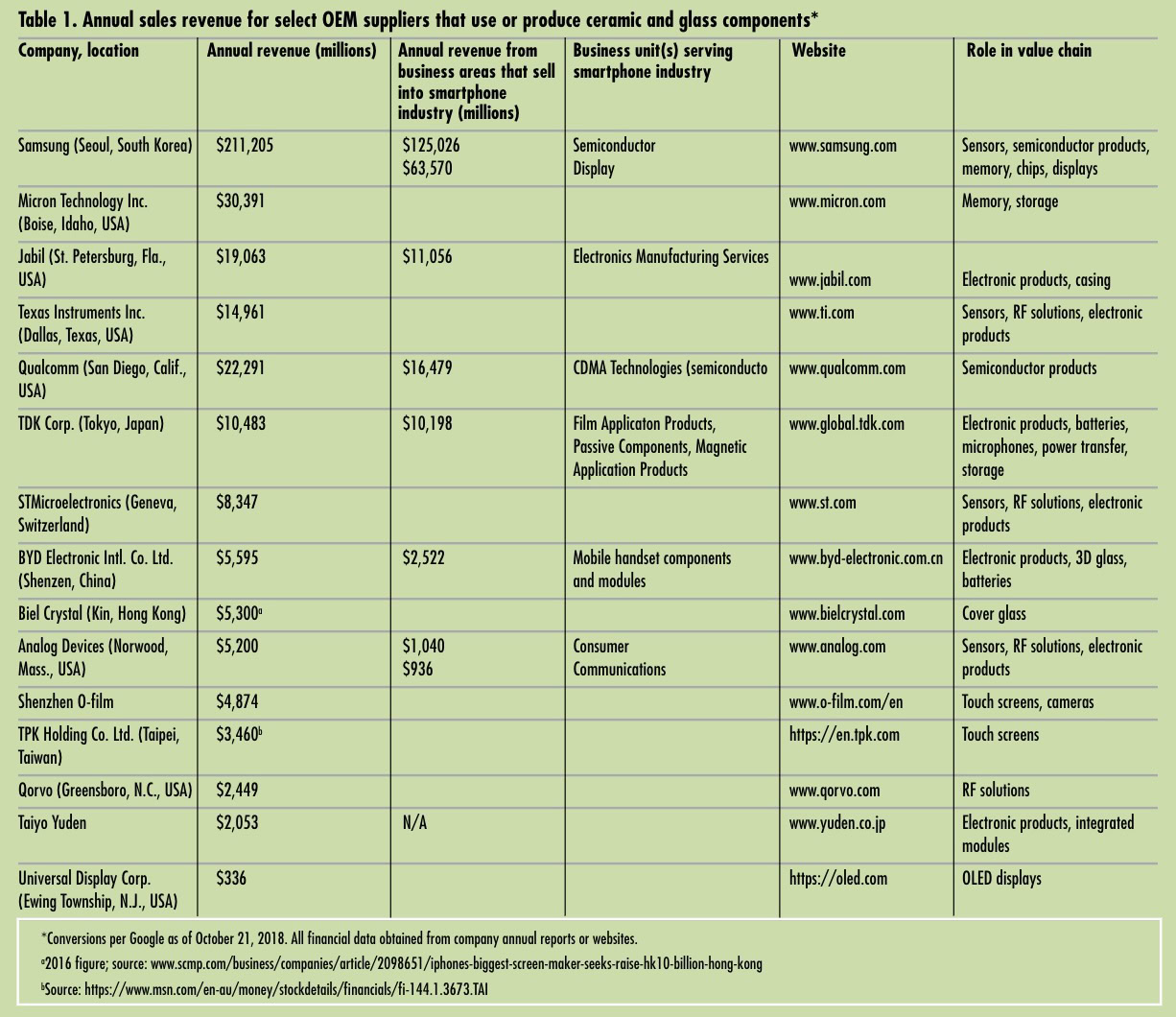

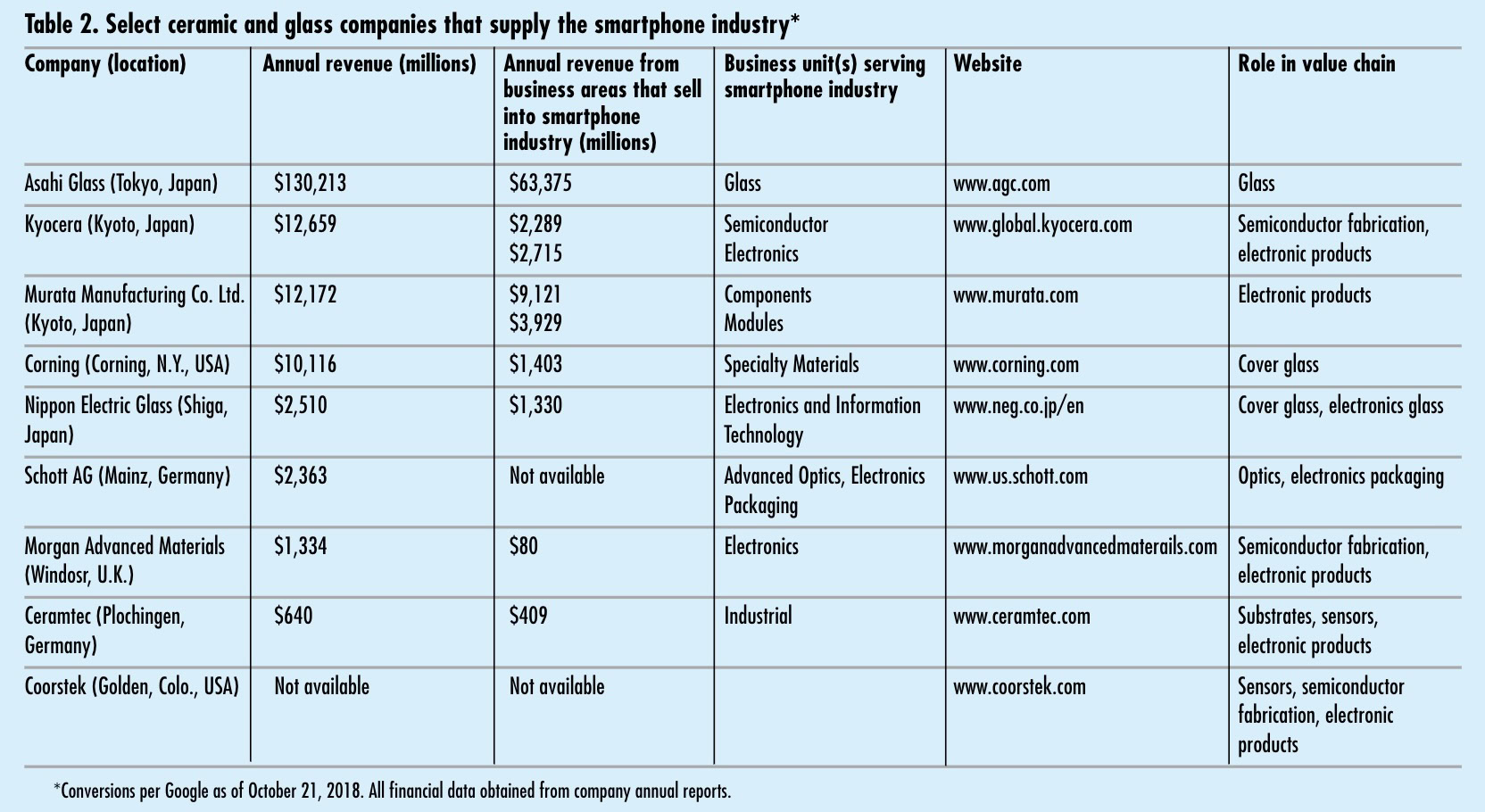

Ceramics and glass contribute to components that directly build a smartphone, including the battery, camera, display, touchscreen, microphone, and speakers (Figures 4, 5). For example, a thin layer of indium tin oxide often enables the touchscreen functionality, and piezoceramics contribute to the speakers’ ability to pump out high-quality sound. Table 1 reports contributions and select OEM companies to the supply chain. Table 2 shows the contributions and select glass and ceramic manufacturers to the smartphone supply chain.

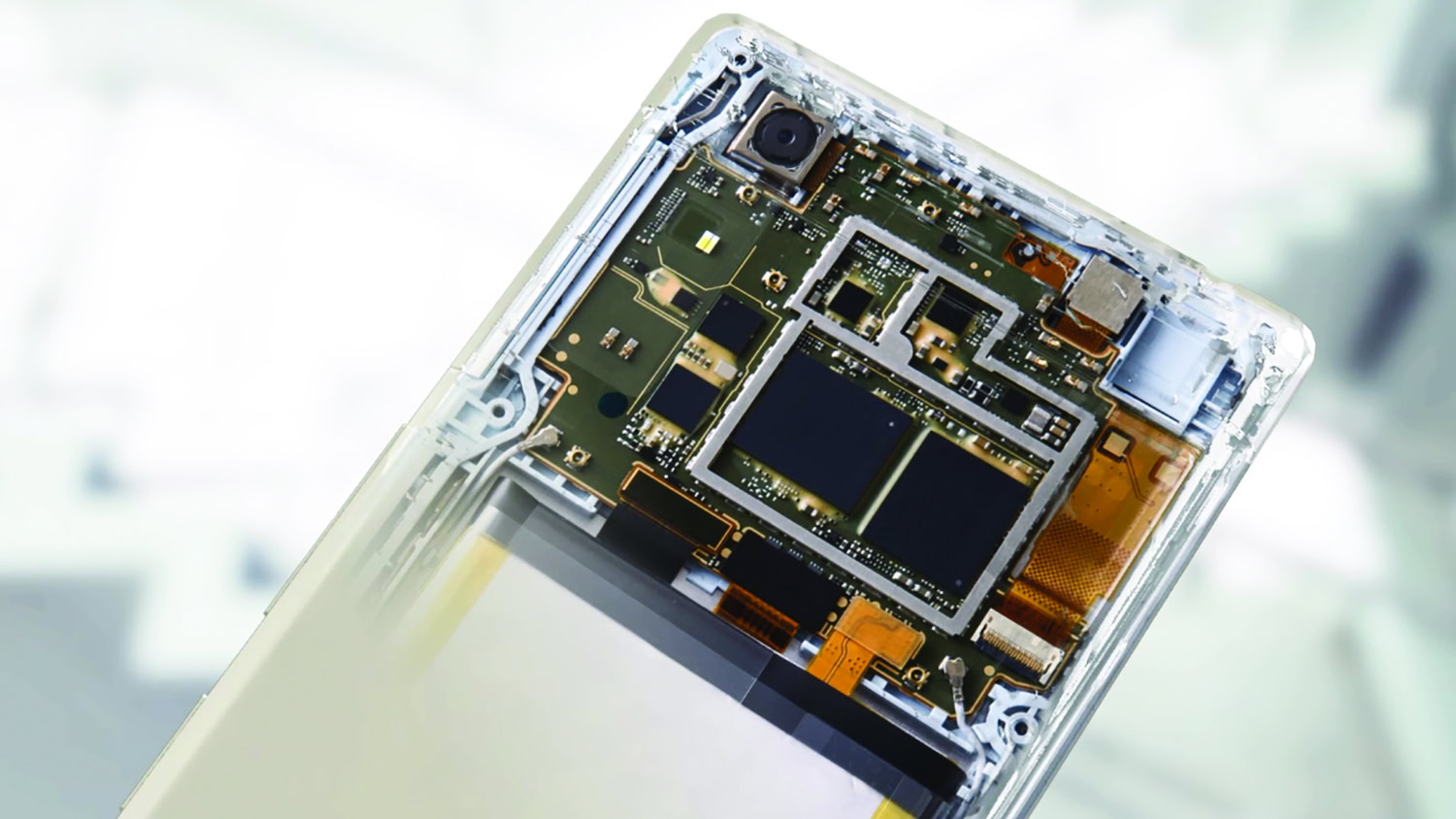

Figure 5. A cutaway view of the internal components of a modern smartphone. Credit: Kyocera Corp.

“About 15 percent of a mobile phone today is made from ceramics and glass—from electronic applications with circuit boards for thermal management to the cores of passive components like inductors, fuses or resistors, all the way to housings and bodies,” says Reinhard Lenk, head of R&D at Ceramtec (Plochingen, Germany), in an interview.

In particular, ceramics and glass are integral to the microelectronics industry, contributing to the individual electronic components of smartphones, including diodes, transistors, resistors, capacitors, transducers, and chip inductors.

The microelectronics market grossed $412 billion in 2017, and “manufacturers are thus experiencing the biggest sales growth since the turn of the millennium” according to a Hannover Messe article.17 With the continued growth of the microelectronics industry, the market for electroceramics reached a value of $8.3 billion in 2016 and is predicted to reach a value of $11.5 billion by 2022, growing at a CAGR of 5.5 percent.18

Dielectric ceramics such as piezoceramics provide antennas, inductors, and other radiofrequency (RF) components that allow the device to send and receive signals from cell towers and connect to wireless networks. Because of the multitude of those signals, smartphones also incorporate various ceramic-based resonators and filters to isolate individual RF signals.

Piezoceramics also enable timers, acoustic elements, actuators, and sensors, which are abundant in modern smartphones and enable some of their most valuable functions.

For example, crystals enable the global positioning system (GPS) to triangulate a device’s position by measuring how long it takes signals to travel from nearby satellites to a device. These crystals were once high-purity quartz, although reduced accuracy from temperature fluctuations forced development of new crystals. Today, temperature-compensated crystal oscillators (TCXOs) have added thermal compensation circuitry and more functionally shaped crystals to improve location accuracy. This location accuracy is an important goal for Kyocera.

“Kyocera’s 26-megahertz TCXO for GPS receivers is engineered to generate precisely 26,000,000 cycles per second with a tolerance of just plus or minus 0.5 ppm,” says Jay Scovie, Kyocera’s director of corporate communications, in an interview. “Advances in components like the TCXO have contributed to a 10-fold improvement in consumer GPS performance in recent years. Location results, originally accurate to within about 10 meters, are now often accurate to within a single meter. Engineers are now targeting another 10-fold improvement, which would bring GPS location accuracy down to an amazing 10 centimeters, or about 4 inches.”

Piezoceramics, like lead zirconate titanate, or crystals, like quartz, are also found in sensors that put the “smart” in smartphone. Sensors allow a smartphone to “sense” the world around it, enabling the devices to perform their most convenient functions, like position sensing.

Smartphones contain multiple position sensors, including proximity sensors and magnetometers in addition to the GPS, to determine location and orientation. Proximity sensors detect how close the device is to other objects, enabling automatic functions like disabling the touchscreen when a smartphone is brought to the face to make a call.

Smartphones also include motion sensors like gyroscopes and accelerometers to detect motion, tilt, vibration, speed, and rotation. These functions allow the phone to detect direction and perform functions like tracking steps. Smartphones contain several environmental sensors, such as barometers, thermometers, and hygrometers, in addition to light sensors like the ambient light sensor that automatically adjusts screen brightness.

Even if not directly present in the components themselves, ceramics also assist in various other aspects of the manufacturing processes that contribute to smartphone components, such as cutting tools, wear resistant parts, stamping punches, die tools, nozzles, spacers, jigs, and more. The materials serve as feedthroughs, couplers, connectors, and heat sinks in a variety of components and are used to insulate, seal, coat, and protect other materials.

Ceramics also serve supporting roles as substrates for various components, including microelectronics, sensors, and actuators. Specifically, cofired ceramics, including high-temperature cofired ceramics (HTCC) and low-temperature cofired ceramics (LTCC), often serve as the base material for substrates and packages for capacitors, inductors, resistors, transformers, hybrid circuits, and more.

These supporting-role ceramics are big businesses. For example, the market for ceramic substrates, driven largely by the electronics industry, is predicted to reach a value of $11.6 billion by 2026, growing at a CAGR of 7.2 percent during 2017–2026.19 According to the market report, “The rising demand for ceramic substrates from several end user industries is a key driving factor for the market. Furthermore, rising adoption of ceramic substrates as an alternative to alloys and metals, miniaturization of electronic devices, rising demand for compact microelectronics packaging solutions such as HTCC and LTCC, and advancements in ceramic substrates are some of the factors boosting the market growth.”

These examples only provide a flavor of the overall contribution of the diverse ways that ceramics and glass contribute to the smartphone industry. A complete list of contributions are beyond the scope of this article, and perhaps any article, to exhaust the entire ecosystem of how ceramics and glass contribute to smartphones.

Critical to the semiconductor industry

In addition to smartphones, ceramics hold a somewhat invisible role in the broader electronics industry through the materials’ diverse and integral contributions to the semiconductor industry.

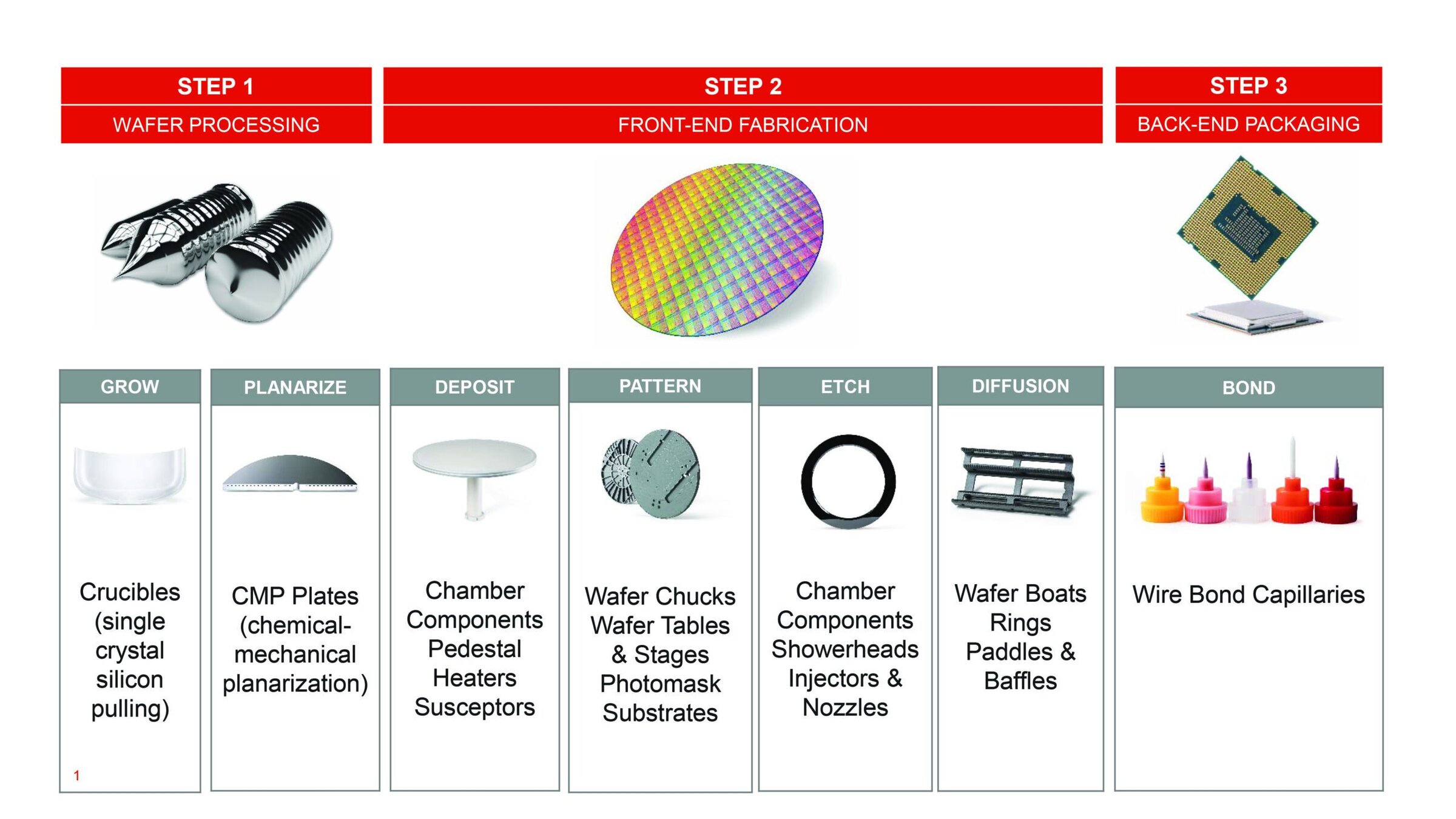

“Ceramics are used in virtually every step of the semiconductor manufacturing process—from silicon wafer processing, to ‘front end’ fabrication, to ‘back end’ packaging,” Randel Mercer, chief technology officer at CoorsTek, says in an interview. “A variety of smart semiconductor ‘chips’ support the broad functionality of today’s smartphones. My iPhone, for example, has more than 20 chips.” CoorsTek develops and manufactures hundreds of critical ceramic components and devices used in the manufacturing of semiconductor devices (Figure 6).

Figure 6. Ceramics are used in virtually every step of the semiconductor manufacturing process—from silicon wafer processing to packaging. Credit: Coorstek

While traditional personal computers contained a motherboard to connect separate, individual components, smartphones demand a more compact package to deliver that same functionality in the palm of your hand. To deliver this compact functionality, smartphones integrate their computing power into a system on a chip (SoC), a single chip that combines a central processing unit (CPU) with processing power for the graphics, camera, audio, and video, often in addition to the devices, memory, modem, and RF functionalities (not all chips are created equally). The SoC is often referred to as the “brains” of a smartphone.

Those chips, like any electronics, start with semiconductor wafers, another place where the contribution of ceramic materials can be found.

For example, Coorstek produces engineered quartz crucibles (Figure 7) that are used at the very beginning of the semiconductor manufacturing process, to melt raw silicon and grow large single crystal boules, which are eventually sliced to generate electronics-grade semiconductor wafers. “These crucibles are complex, multilayered composites of different materials that allow for low defect silicon crystal growth,” Mercer says.

Figure 7. Coorstek produces engineered quartz crucibles that are used to melt raw silicon and grow large single crystal boules for the semiconductor industry. Credit: Coorstek

Once the wafers are made, additional advanced ceramic components are used for wafer handling and fabrication processes, such as deposition, lithography, etching, and diffusion. The corrosion resistance of ceramics makes them well-suited for wafer polishing substrates, chucks and carriers, heaters, plasma-resistant parts, nozzles, windows, and feedthrough insulators.

Ceramic components can also be found in a vast array of semiconductor wafer fabrication equipment, where they contribute to every part of the fabrication process. In fact, the market for ceramics in wafer fabrication equipment is estimated at about $350 million.16

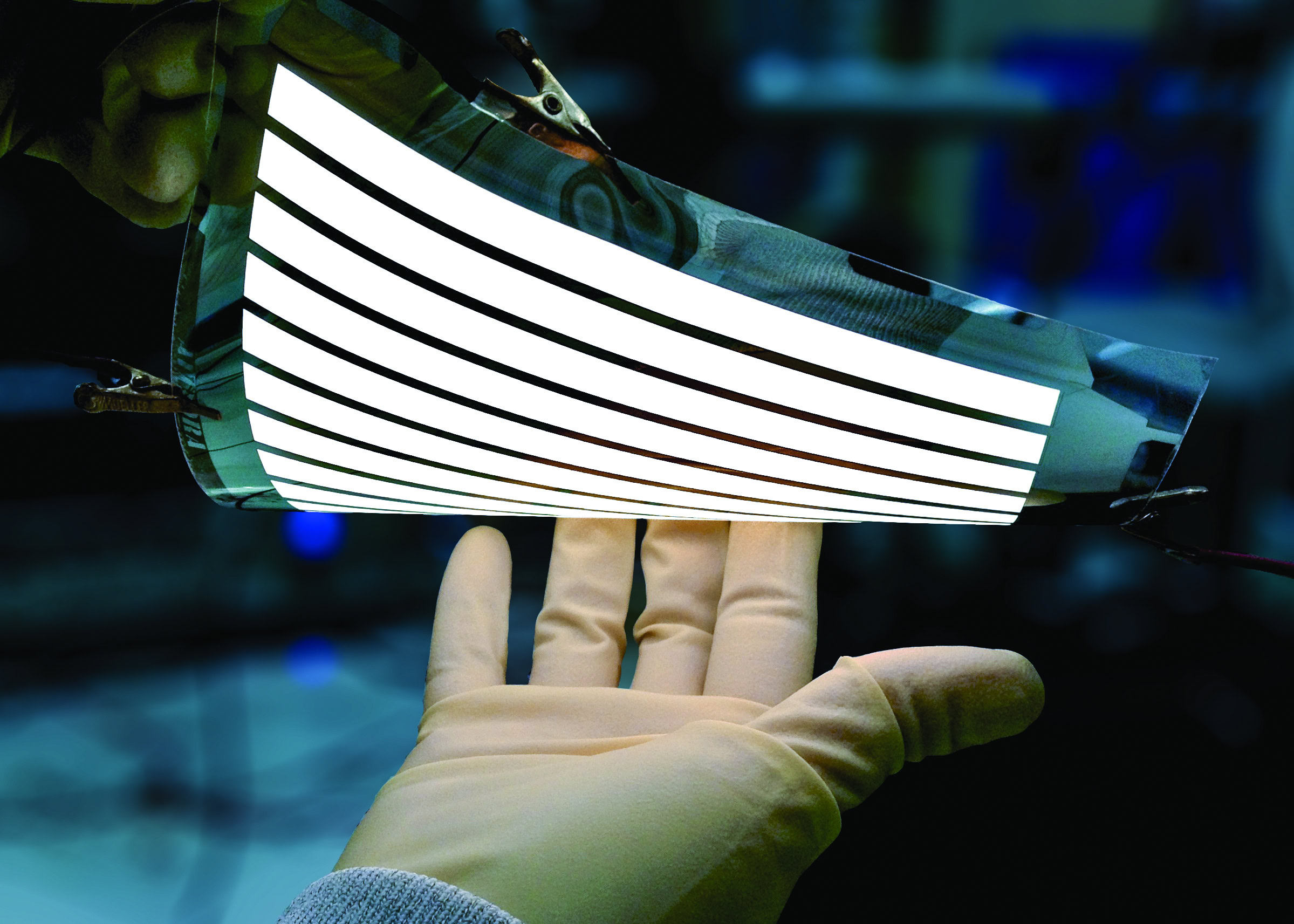

“To support critical patterning technology, CoorsTek also synthetically grows large quartz sheets via chemical vapor deposition (CVD) to achieve high optical clarity and low chemical impurities,” Mercer adds. “This CVD quartz is machined and polished into quartz plates that can be as large as a queen size bed and become the optical reticles used for patterning the circuitry on flat panel display glass, which is then diced up to produce television screens and smartphone screens.” (Figure 8).

Figure 8. CoorsTek synthetically grows and processes large quartz plates that become optical reticles to pattern the circuitry on display glass. Credit: Coorstek

Ceramics also serve as substrates, packaging materials, and other supportive roles in the semiconductor industry. While more secondary to the final manufacturing product, these functions are nonetheless critical enabling technologies.

“Within a typical smartphone, there are hundreds of tiny wires that connect the semiconductor chips to packages and circuit boards,” Mercer explains. “CoorsTek Gaiser® ceramic capillaries are used to provide strong, high reliability wire bonds (Figure 9). These ceramic bonding tools deliver the improved durability needed to help the industry transition from the use of expensive gold wire to more economical but harder copper wire, providing dramatic cost savings.”

Figure 9. Coorstek manufactures ceramic capillaries that are used to provide the wire bonds that connect semiconductor chips to packages and circuit boards. Credit: Coorstek

Although these examples demonstrate only a few places where ceramics integrate into the semiconductor industry, the total contribution of ceramics to the semiconductor industry mirrors the extensive contributions to smartphone industry overall.

Beyond sheer scale, that contribution constantly evolves with the technology. With smartphones, that may be even more true as market slowdown and saturation prompts smartphone suppliers to increasingly rely upon added features and improved functionalities to sell new devices.

That evolution consequently ripples through all other industries connected to the smartphone market—so how are trends in the smartphone industry shaping the future of the ceramics and glass industries?

Displaying the future

“With the ongoing fight at the high end, vendors will need to find a way to innovate ahead of the curve to attract new users and increase shipments while driving profits,” according to an International Data Corporation news release.20 “The display looks like it could be the next battlefield for the smartphone over the next couple years. … As smartphone owners continue to consume media on their devices, the screen (bigger, brighter, and bolder) will be an integral part of the overall design language for each vendor.”

This statement may not be surprising when you consider that the display is often one of the most expensive components in a modern smartphone. A teardown analysis of the iPhone X reveals the total cost of component materials is $370.25. Almost a third of this cost, $110, is accounted for by the display and touchscreen module alone.21

Smartphone displays use two different technologies: liquid crystal display (LCD) or organic light emitting diode (OLED), both of which were originally deposited on glass substrates and, as electronic technologies, contain ceramic materials. LCD screens have reigned supreme for many years due to their low cost; OLEDs will provide higher image and color quality, but at a higher price.

According to Universal Display Corporation, a leader in electronics OLED displays, OLEDs currently account for about 400 million displays of the roughly 1.5-billion-unit annual smartphone market. Market analysis predictors indicate that OLEDs trend upwards, and will likely comprise 58 percent of smartphone display shipments in 2019.22

That trend can be partially attributed to recent developments that have allowed OLED displays to become thinner and lighter. “One of the trends now in particular for OLEDs is that we don’t have to be limited to glass—displays can now be fabricated on plastic,” Mike Hack, vice president of business development for Universal Display Corporation, says in an interview. “There have been a lot of technical challenges in getting to that point.”

One of those challenges is that OLEDs are sensitive to oxygen and moisture. “Glass is a barrier to oxygen and water. But if you move to plastic, you need to develop an encapsulation film that is very thin, transparent, flexible, and cheap,” Hack says, to protect the OLEDs from degradation.

The display industry has been working on this challenge over the past decade and has now commercialized relevant technology within the past few years. These encapsulation films consist of a multilayer structure of ceramics and organic materials that together provide flexibility and serve as an effective barrier. Sandwiching an OLED in between these multilayer encapsulation films prevents oxygen and moisture from reaching the OLED and degrading the display (Figure 10).

Figure 10. A flexible OLED panel manufactured by Universal Display Corporation. Credit: Universal Display Corporation.

As an alternative to plastic, flexible glass is also another option for display substrates, Hack says. “Even in terms of glass, there are a lot of new glasses today that can be considered as a substrate.”

However, plastic substrates have an edge when it comes to affording another freedom of form factor: rollable or foldable displays.

“The next wave of inflection in smartphone technology will be foldable phones, something the size of a tablet that you can fold in half or in thirds so it’s the size of a phone,” according to an article published in The Optical Society’s Optics & Photonics News.23 “Every major display maker is in an intense race to see who can release it first. It’s only a matter of time before the first foldable phone hits the market.”

Samsung, a global leader in the smartphone and electronics markets, could be the first to unveil foldable devices to the world. The company is reportedly developing a Galaxy X model, expected for release in 2019, that will have a display that unfolds for tablet-like functionality. Design speculations indicate the device will unfold like a wallet, opening up to reveal a total display that stretches more than 6.5 inches across.24

While foldable AMOLED displays are expected to represent about 0.001 percent of flexible AMOLED shipments in 2018—itself representing only a portion of the overall display market—that figure is predicted to rise to 6 percent in 2021.25

Once consumers catch on to the idea of smartphone sized devices that offer tablet functionality, foldable displays will take off, Hack predicts. “It’s going to take some time, but will be a major shift in what our devices look like in the next few years.”

Clear innovation

Foldable displays present new materials challenges, particularly in regard to the cover screen, which has long been dominated by glass. One important consideration is the materials tradeoff between flexibility and durability, which could indicate a limited market for foldable displays.

“Display attributes will continue to dominate what materials are used in these devices, which drives back to a core set of properties—scratch resistance, optics and transmissivity, and durability in drops,” says Scott Forester, division vice president for marketing and innovation products within Corning’s Gorilla Glass business, in an interview. “Those, at the end of the day, come back to a glass solution.”

The success of Corning’s durable Gorilla Glass formulation—which uses an ion-exchange process to create compressive stress and increase the glasses’ durability—has positioned Corning to command an estimated 40 percent of the display glass market. Nippon Electric Glass and Asahi Glass each capture 25 percent of the market (CNBC report).26

That market for global smartphone cover glass is expected to grow from $1.41 billion in 2017 to $1.57 billion in 2023, a CAGR of 1.9 percent.27

Corning announced its newest iteration of damage-resistant cover glass, Gorilla Glass 6, in July 2018. Gorilla Glass 6 offers even higher compressive strength and durability than previous iterations of Gorilla Glass, all of which are big improvements over traditional soda-lime glass.

According to Corning, the improvement is necessary because people tend to drop their phones about seven times per year, from an average drop height of one meter—about waist height, the ideal place for a phone to take a dive from a pocket, purse, or hand. Corning precisely designed Gorilla Glass 6 to stand up to this daily abuse.

Corning’s lab tests show that the new Gorilla Glass formulation is so strong that it can survive an average of 15 consecutive 1-meter drops onto rough surfaces and “is up to 2x better than Gorilla Glass 5.”28

“We were able to not only change the glass composition to make it more optimized, but we also were able to change the ion exchange process to basically have an end result that puts a greater stress profile into the glass,” Forester says. That stress profile—a plot of compressive strength and depth of layer—shows that Gorilla Glass 6 increases the area under the curve by more than 30 percent, achieving much higher compressive force at the surface.

More durable glass has an added benefit beyond being able to better survive drops and abuse. The glass can now assume bigger sizes and more complex shapes.

This larger size and shape ability is fortunate for glass, because smartphone displays are getting bigger. While 5.5–6 inch screen sizes only accounted for 7.5 percent of the smartphone market in 2014, they accounted for 43.3 percent of screens as of 2017, a CAGR of 19 percent.29 The trend is expected to continue through 2021, with screens of 5–6 inches commanding almost 85 percent of the smartphone screen market in 2021.

Smartphone displays are maximizing available space, too. Trends continue for the display to take up more of the available screen real estate, with displays that stretch to the edges of devices and eliminate the bezel (the “frame” between a display and the physical edge of a device).

These display evolutions require cover glass to assume new shapes. Devices are increasingly incorporating 2.5-D displays, in which the edges of the cover glass are rounded, and even 3-D displays, where the cover glass wraps around the sides of the device. “That of course puts new challenges on the glass itself to be more durable in those situations,” Forester says.

2.5-D and 3-D cover glass shipments are expected to drive growth in the smartphone market, as manufacturers and designers try to integrate new features to stimulate new device sales. While 3-D cover glass is expected to make up just 3 percent of the market in 2016, that segment is expected to grow to almost 8 percent of the market in 2018, when 2.5-D will account for almost 44 percent and 2-D will account for about 48 percent of the cover glass market.30

Challenges in making glass durable in these new shapes, and the added difficulty in simply manufacturing glass in more complex shapes—combined with predicted trends for foldable displays—could offer opportunities for alternative materials such as plastic in the cover screen market.

Futuristic functionalities are today’s features

The increase in the amount of time that users spend on smartphones and the trend for bigger and better displays hints at one important point about smartphones: we are using these electronics devices to do more in our daily lives.

Smartphone suppliers continue to add additional functionalities to their devices as a consequence of rapidly evolving technologies—including screenless displays, augmented and virtual reality, artificial intelligence, and increased interactions with the Internet of Things (IoT). These functionalities ultimately can be traced back to materials advances themselves.

Screenless displays are already beginning to appear, although the current demonstrations have a way to go before they are incorporated directly into devices. The world’s first holographic call made its debut in September 2018 at the Mobile World Congress Americas, technology brought to the show floor by Voxon Photonics and Verizon 5G.31 The video conference call projected the caller’s holographic face, and users on the call viewed and manipulated a set of holographic medical images.

This technology could represent an oncoming evolution in the future of displays, as some analysts predict screenless displays will eventually replace touchscreens.32 The total market for screenless displays is expected to explode within the coming years, growing at a CAGR of 33.7 percent to reach a predicted value of $3 billion by 2023.33

Other high-tech functions that once seemed science fiction are also finding their way into smartphones. Many smartphones already feature some early forms of augmented reality, which is predicted to represent a quickly growing trend.

Total spending on augmented reality and virtual reality around the globe is expected to at least double every year through 2021, reaching $215 billion in 2021.34 At a CAGR of 113.2 percent during 2017–2021, that’s incredible growth that represents sizeable potential for added and enhanced functionalities in smartphones and beyond.

Artificial intelligence, enabled by the addition of neural processing units into smartphones, has already found its way into most models, although the intelligence is predicted to continue to learn, getting better at processes like classifying and identifying photos, automating calendar entries, and making useful location-based suggestions. The mobile artificial intelligence market is predicted to be worth $17.83 billion by 2023, growing at a 28.41% CAGR from 2018–2023.35

While these added functionalities are prime features for smartphone suppliers to use as selling points for new devices in a slowing market, the added abilities of smartphones affect the very materials that enable them, too. Ultimately, as component needs change in the fast-paced smartphone market, the component materials, designs, and manufacturing process must keep up as well.

Credit: Verizon; YouTube

Shrinking sizes, merging functions

So how did we get to this point—smartphones that have evolved to seemingly do everything yet have remained small enough to fit in your hand? There are two answers—miniaturization and integration.

“Miniaturization involves making electronic components smaller with each new generation—helping to shrink your computer, flatten your home-theater TV, and downsize circuits into wearable or implantable dimensions,” Kyocera’s Scovie says.

Smartphone manufacturers have seized the opportunities miniaturization offers.

“One of the key enablers is the miniaturization of the integrated circuit with feature sizes shrinking from 1 µm in the 1980s to 10 nm today,” a CoorsTek spokesperson says. “Smartphones exemplify this progress. The computing power in a standard smartphone today far exceeds that of any commercially available computer from just a couple decades ago, in a fraction of the footprint.”

The smaller sizes of those components, in turn, allow more functionality to be squeezed tighter together—in other words, integration.

“In simple terms, integration involves making one circuit board serve multiple functions by incorporating these smaller components into denser circuitry of more sophisticated design,” Scovie explains. A prime example of integration in smartphones is the system on a chip (SoC).

Ultimately, miniaturization and integration have worked together to enable the advances that make modern smartphones the devices they are today—but how?

“Advanced materials are the key drivers of miniaturization and integration, the two trends in modern electronics that make the smartphone possible,” Scovie says.

In general, materials and manufacturing communities have gotten better at making things, making them at smaller sizes, and making them more economically—enabling more functionality to be packed into a smaller capacitor, inductor, or processor, for example.

“Designing material properties is not only a result of the materials’ composition, but also is very connected with manufacturing processes as well,” Ceramtec’s Lenk says. “For example, ceramic cores for electrical resistors have been miniaturized over years. It’s not only the material itself, but the manufacturing processes—which Ceramtec helped adapt—that have played a role.”

Together, advances in the materials and components, through both improved design and manufacturing processes, mean that smartphones today have drastically increased their capabilities without a consequent increase in their size.

Can you hear me now?

Those increased capabilities, combined with the increased device use that they precipitate, translate into a large demand for mobile data.

Global mobile data traffic is predicted to double from 24 exabytes (1 exabyte = 1 billion gigabytes) per month in 2019 to 49 exabytes per month by 2021.36 On an individual basis, a recent report indicates that mobile users in the United Kingdom consumed an average 1.9 GB of data per month in 2017.37

The sheer volume of this data is astonishing, but even more astounding is that this data is being transmitted wirelessly, meaning that exabyte upon exabyte of data is constantly flowing around the globe via RF signals.

And those figures only represent mobile transmissions. Once a predicted 25 billion IoT connections are floating through the airwaves by 2025,6 it will be a wonder that any device will be able to make sense of the sea of RF signals.

Modern smartphones integrate increasingly complex RF antenna designs, consisting of several different kinds of antennas that use more frequency bands across a wider bandwidth. Such strategies support functions, like expanded carrier aggregation, to increase data capacity.

Carrier aggregation combines multiple frequency bands to increase network performance, but also requires antennas to simultaneously operate across multiple bands.

As with nearly every smartphone component, the trend is to add capacity, increase efficiency, and reduce size—a challenge for the component and its materials.

In addition to the design and materials of the RF system, a smartphone’s casing material and bezel design also impact RF performance. And because ceramic and glass materials cause less RF interference than metal, these materials are increasingly gaining adoption as casing materials. Glass backs also enable wireless charging, another trending feature. According to a Tech Republic article, 28 percent of phones sold in 2018 have a glass back.38

While the antenna is an important component of smartphones, it is only one part of a device’s entire RF system. An additional critical component is the RF front-end, positioned between the RF transceiver and antenna, which consists of power amplifiers, low noise amplifiers, switches, duplexers, filters, and other components. The RF front-end does much of the work to process signals and make sense of them with the vast RF signal sea, ultimately enabling the correct signal to reach its intended target.

“Most smartphone users today aren’t even aware of what the RF front-end is, but it has remained one of the most critical aspects of mobile handset design since the product’s inception,” says Wayne Lam, principal analyst of mobile devices and networks for IHS Markit, in a market insight article.39

“To help accommodate expanded band support in as little space as possible, the RF front-end is becoming increasingly modular with more power amplifier, filter, duplexer, switch, and low noise amplifier content being incorporated within front-end modules than ever before. As components are combined into modules and the component density of the printed circuit board allocated for the RF front-end rises, interference between components becomes more of an issue and the challenges of each RF component achieving adequate isolation intensifies.”

In other words, the RF front-end is increasingly integrated, which in itself causes additional materials challenges. The issue of interference requires an increasing number of filters to isolate particular RF signals and filter out unwanted signal noise.

The number of filters has grown from less than 10 per high-end phone in the early 2000s to more than 60 filters per device as of 2015, “…and this will move toward 100+ in the future as high-end technology becomes more mainstream for mid- and low-cost smartphones,” writes Rich Ruby of Avago Technologies (Sans Jose, Calif.) in a 2015 article in IEEE Microwave Magazine.40

“The math becomes staggering: 2 billion (or more) smartphones sold per year? Then, 50–200 billion filters per year or more? Avago estimated that world capacity for mobile filters was on the order of 20 billion in 2013. The growth rate (and even the possibility that demand could outstrip supply) makes filters a very interesting technology—whether purely for their technical tour de force or for the potential economic impact.”

The increasing number of filters that must be integrated into high-performance devices like smartphones has consequently meant that filters needed to go on a drastic diet to shrink in size.

Combining a continual demand for higher performance and shrinking size along with an added demand for reduced energy consumption (the display and RF system are the largest users of power in the average smartphone) means that these filters face considerable materials challenges, too.

One large step forward in addressing some of those challenges came with the development of piezoelectric-based resonators, particularly surface acoustic wave (SAW) and bulk acoustic wave (BAW) filters. These high-performance acoustic filters—predominantly composed of a thin film on aluminum nitride (AlN)—provide greater signal isolation and improved performance in a much more compact package that their bulky ceramic monoblock predecessors.

In particular, development of a BAW device called a free-standing bulk acoustic resonator (FBAR) significantly advanced the technology. “In 2001, FBAR duplexers forever changed the shape of phones by eliminating the large ceramic block duplexers needed to perform the function of separating the transmit signal from the receive signal,” according to a 2012 article in the MRS Bulletin.41 Duplexers instead permit simultaneous signal transmission and reception—providing yet another example of both miniaturization and integration.

More recently, scandium-doped AlN is making its way into device resonators, as the material offers still higher performance.

Phoning the future

The story so far of smartphones is one of meteoric rise, unprecedented infiltration, and amazing technology, and it is a story that could not be told without the contributions of ceramic and glass materials.

“Together, miniaturization and integration explain why today’s typical smartphone can function as a phone, computer, web browser, retail purchase point, GPS navigation system, media player, camera, video camcorder, voice recorder, language translator, TV, calendar, calculator, stopwatch, timer, alarm clock, address book, game console, and flashlight—all in the palm of your hand,” says Kyocera’s Scovie.

This statement raises an interesting point—materials-based advances have enabled the smartphone to become the device it is today, a device with such incredibly increasing functionality that it is, in turn, demanding further advances in the very enabling materials themselves.

The entire ecosystem represents a continually evolving cycle of innovation. Constant forward momentum will continue to stimulate development of ever more sophisticated materials that can improve function while reducing size and weight, pushing the technology ever further.

Even though ceramics and glass contribute roughly 15 percent of the material in an average smartphone, the impact of ceramic and glass materials on the smartphone industry is much more significant. Ceramics and glass have already supported giant leaps in the technology that has enabled the modern smartphone—and the materials will surely continue to rise to the challenge to enable the devices of tomorrow.

Related Articles

Market Insights

Engineered ceramics support the past, present, and future of aerospace ambitions

Engineered ceramics play key roles in aerospace applications, from structural components to protective coatings that can withstand the high-temperature, reactive environments. Perhaps the earliest success of ceramics in aerospace applications was the use of yttria-stabilized zirconia (YSZ) as thermal barrier coatings (TBCs) on nickel-based superalloys for turbine engine applications. These…

Market Insights

Aerospace ceramics: Global markets to 2029

The global market for aerospace ceramics was valued at $5.3 billion in 2023 and is expected to grow at a compound annual growth rate (CAGR) of 8.0% to reach $8.2 billion by the end of 2029. According to the International Energy Agency, the aviation industry was responsible for 2.5% of…

Market Insights

Innovations in access and technology secure clean water around the world

Food, water, and shelter—the basic necessities of life—are scarce for millions of people around the world. Yet even when these resources are technically obtainable, they may not be available in a format that supports healthy living. Approximately 115 million people worldwide depend on untreated surface water for their daily needs,…