Nonferrous metals serve foundational roles in the electrification, renewable energy, and digital transformation.

Nonferrous metals are metals that do not contain iron in significant amounts. These metals typically are nonmagnetic, corrosion resistant, electrically and thermally conductive, and lightweight, making them ideal for applications in the emerging markets mentioned above.

Even as demand for these metals surges, supply chains face geopolitical and environmental challenges. Overcoming these challenges will require innovations in various sectors, including the development of advanced refractories to deliver high-quality materials through safe and effective metallurgical processes.

Market momentum: Nonferrous metals powering global growth

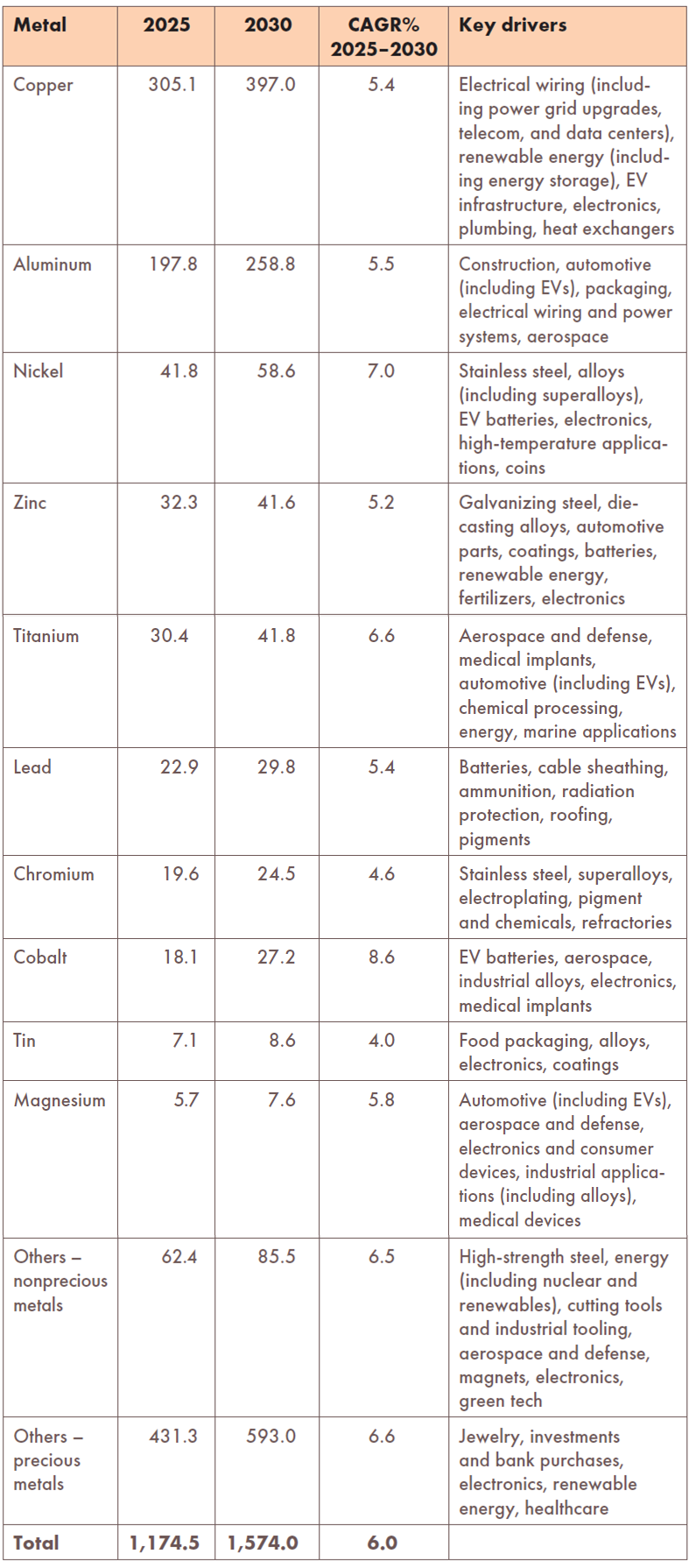

Of the more than 90 nonferrous metallic elements on the periodic table, only about 10 have significant importance in industrial applications (Table 1). In 2025, these top metals accounted for more than 90% by volume and 58% by value of the nonferrous metals market, with aluminum and copper leading the charge.

Aluminum demand is nearly three times that of copper; however, as seen in Table 1, the copper market is larger in value because of copper’s much higher unit price. As of the end of 2025, copper traded at roughly four times the price of aluminum.

Table 1. Nonferrous metals market by metal, 2025–2030 ($ in billions). Table data was independently obtained by specialty market research firm AMG NewTech.

The total market value for nonferrous metals, including precious and nonprecious metals, is projected to have healthy growth during the next five years, rising at a compounded annual growth rate (CAGR) of 6.0%, from $1.2 trillion in 2025 to $1.6 trillion globally in 2030.1,2 The key growth drivers for this market are as follows:

- Urbanization: Expansion of cities and infrastructure worldwide is creating greater demand for components such as aluminum windows, copper plumbing, and transportation-related elements.

- Electrification: Transition to electric power in transportation and industry is in progress. Nonferrous metals are essential for electrical wiring, motors, power transmission lines, electric vehicle (EV) batteries, and energy storage systems. As an example, an EV uses 80 kg of copper versus 23 kg in a conventional car.3

- Sustainability: There is growing pressure to reduce carbon footprints and adopt greener technologies. Nonferrous metals enable production of lightweight structures that improve fuel efficiency and are critical in renewable energy systems such as solar panels and wind turbines. Global decarbonization policies are creating unprecedented demand for nonferrous metals.

- Recycling: The emphasis on circular economy and resource efficiency is intensifying. Nonferrous metals are highly recyclable without losing their properties, allowing for lower manufacturing costs and a reduced environmental impact.

Although aluminum and copper are projected to maintain the dominant share of the nonferrous metals market during the next five years, the markets for cobalt, nickel, and titanium will expand more rapidly because of their critical role in emerging technologies and strategic industries.

Cobalt and nickel are essential for lithium-ion batteries used in EVs and renewable energy storage systems, which drive the global energy transition. Other key applications of these two metals include superalloys for turbines and jet engines, which like the energy applications are experiencing exceptional market growth worldwide, thus creating unprecedented demand. Titanium is also increasingly demanded in aerospace and defense applications due to its exceptional strength-to-weight ratio and corrosion resistance.

Nonferrous metals are not only vital to industry but also in applications that save lives. Titanium and cobalt alloys are revolutionizing implants, surgical instruments, and advanced medical devices, enabling innovations in orthopedic surgery, cardiovascular stents, and diagnostic technologies.

Supply chain volatility, regulatory pressures, and energy costs

Despite the increasing demand for nonferrous metals, this market faces some major challenges: supply chain volatility, environmental regulations, and energy costs.

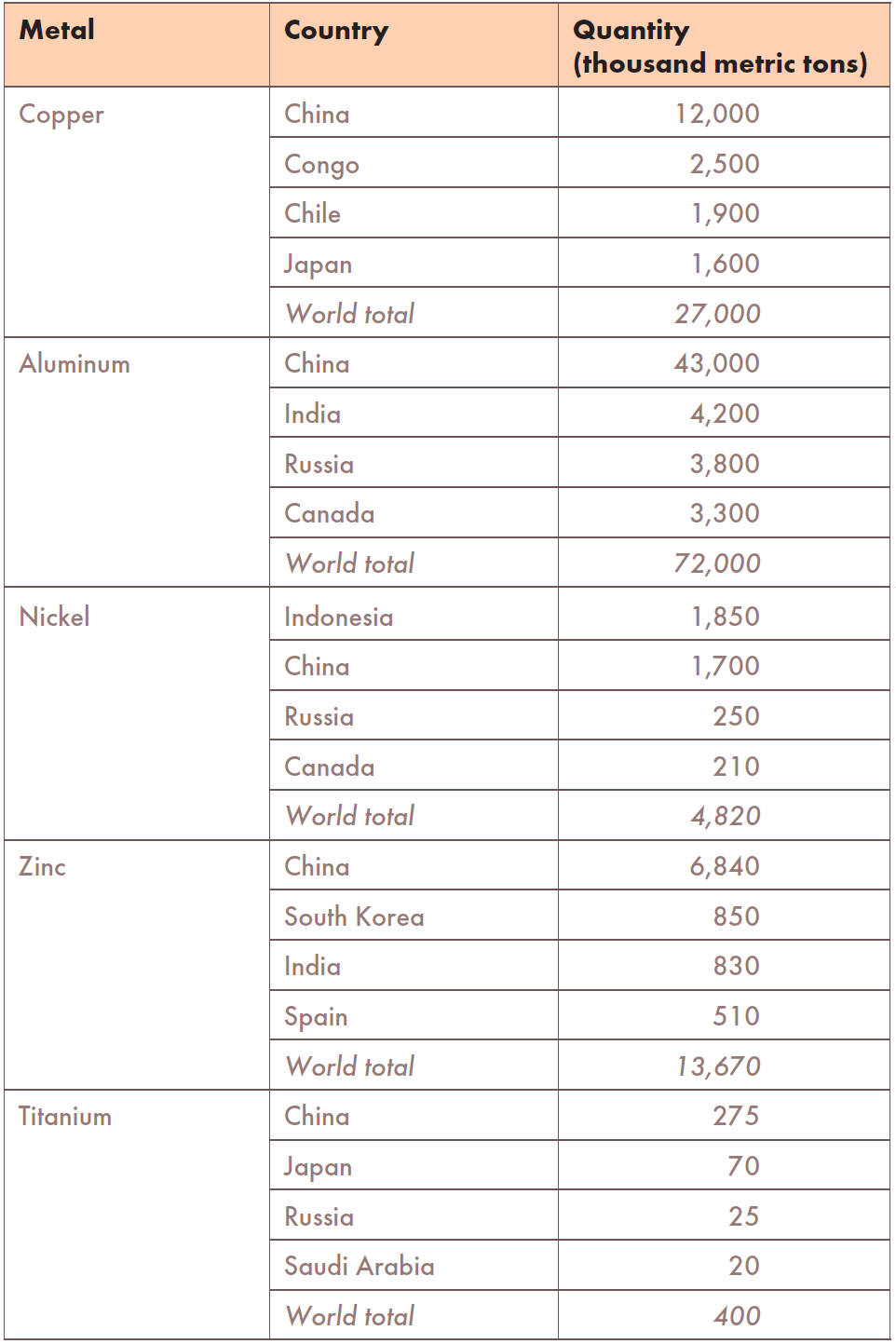

Nonferrous metals typically are sourced from geographically concentrated resources. For example, as seen in Table 2,4–11 China produced 44.4% of worldwide copper and 59.7% of aluminum metal in 2024, while Indonesia accounted for 38.4% of nickel production (these figures include both primary and secondary metals). Other key producers of nonferrous metals are India, Russia, Canada, Democratic Republic of the Congo, and Chile.

Table 2. Top producers of common nonferrous metals in 2024 (based on both primary and secondary metals). Table data was compiled by AMG NewTech based on various sources (References 4–11).

In 2025, Chile’s copper output slowed as Santiago-based Codelco, one of the world’s largest copper producers, faced operational setbacks, including a major tunnel collapse at El Teniente mine and declining ore grades across several sites. At the same time, new mining regulations, which were introduced in the country to streamline permitting, also reinforced compliance rigor by requiring standardized evaluations and digital traceability.12 These events underscore the persistent supply risks and regulatory pressures in key producing regions.

Political instability, trade restrictions, and logistics disruptions are additional causes of sudden price spikes, while global events, such as pandemics and conflicts, amplify risks for raw material availability and shipping. As a result, the United States and its allies are promoting initiatives aimed at increasing internal supply. Copper, aluminum, nickel, zinc, and titanium are on the U.S. 2025 List of Critical Minerals,13 triggering stockpiling and diversification efforts.

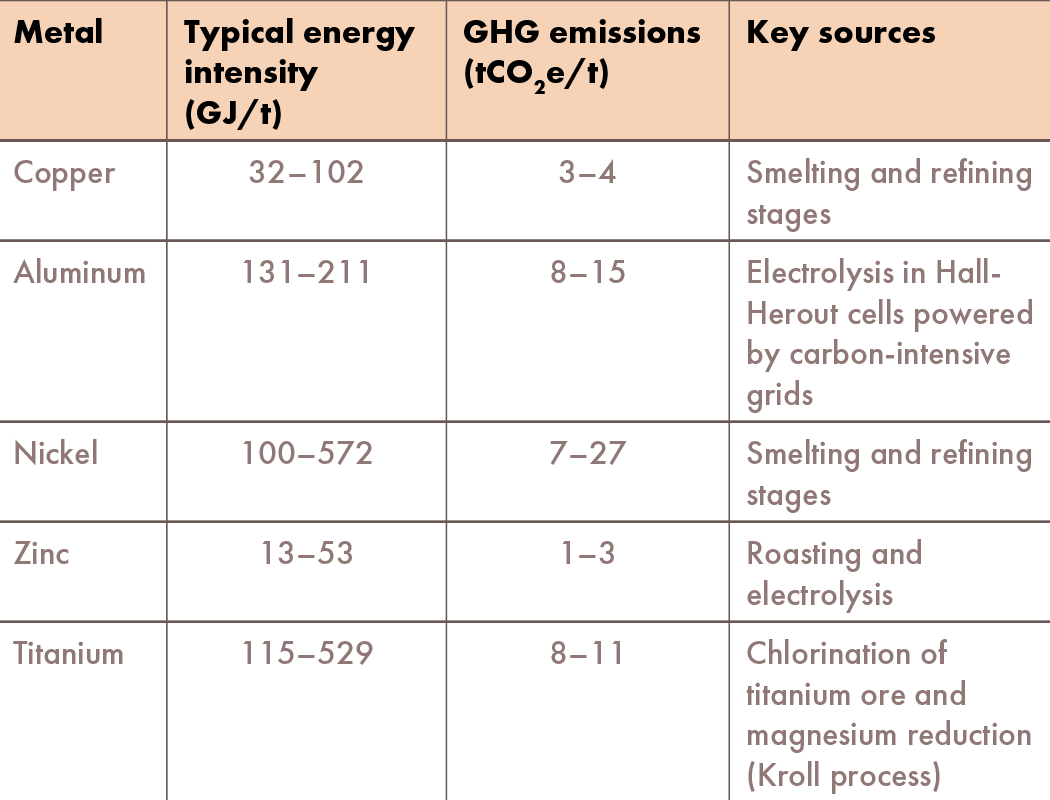

Current production of nonferrous metals relies primarily on traditional high-temperature smelting processes because these methods are very cost effective and scalable (see sidebar “Metals production: Why refractories are essential”). However, these traditional manufacturing techniques are energy intensive and generate substantial emissions and waste (e.g., red mud from alumina refining and CO2 from smelting). These pollutants are subjected to increasing regulatory scrutiny, while rising energy prices inflate production costs and erode competitiveness.

Table 3 shows the energy intensity and greenhouse gas emissions (GHGs) for the primary processes used to manufacture the top five nonferrous metals.14–23 Values change quite broadly based on the specific method used, but most of them greatly exceed the typical energy and emissions values for steel (22 GJ/t and 2.3 tCO2e/t, respectively).14 Primary aluminum, for example, requires at least six times more energy than steel, while its fabrication process releases more than three times the amount of GHGs.

Table 3. Energy intensity and greenhouse gas emissions per ton of common nonferrous metals (primary process). Legend: GJ/t = Gigajoule per metric ton of metal; tCO2e/t = metric ton of CO2 equivalent per metric ton of metal. Table data was compiled by AMG NewTech based on various sources (References 14–23)

Environmental and corporate responsibility regulations also address wastewater discharges from metal manufacturing; effluent limits and pretreatment standards for nonferrous metals forming; restrictions on exporting metal scrap to countries lacking equivalent environmental and social standards; exposure limits for fumes, dust, and other hazards during manufacturing and recycling; as well as best practices for air emissions, noise control, and worker safety.

The effect of these regulations is nuanced because even though they can enable long-term opportunities, such as healthier work environments and more secure supply chains, they can create constraints that hamper production in the short term. Short-term constraints include higher compliance costs and delays as well as carbon taxes and decarbonization mandates. Furthermore, due diligence expenses, or the costs incurred during the investigation phase before approving new projects, delay procurement and contribute to slower approvals, higher initial costs, and supply chain bottlenecks.

Overcoming these challenges and building a resilient supply chain requires action on multiple fronts. As Charles Johnson, president and CEO of the Aluminum Association, notes in an Aluminum Association press release,24 “Even if we could flip a switch and turn on every idled aluminum smelter tomorrow, the U.S. industry cannot currently produce nearly enough metal to make the products that Americans rely upon. … greater self-sufficiency will require an all-of-the-above approach to energy, trade, and recycling policy to ensure that U.S. manufacturers have abundant, affordable metal.”

Innovation in action

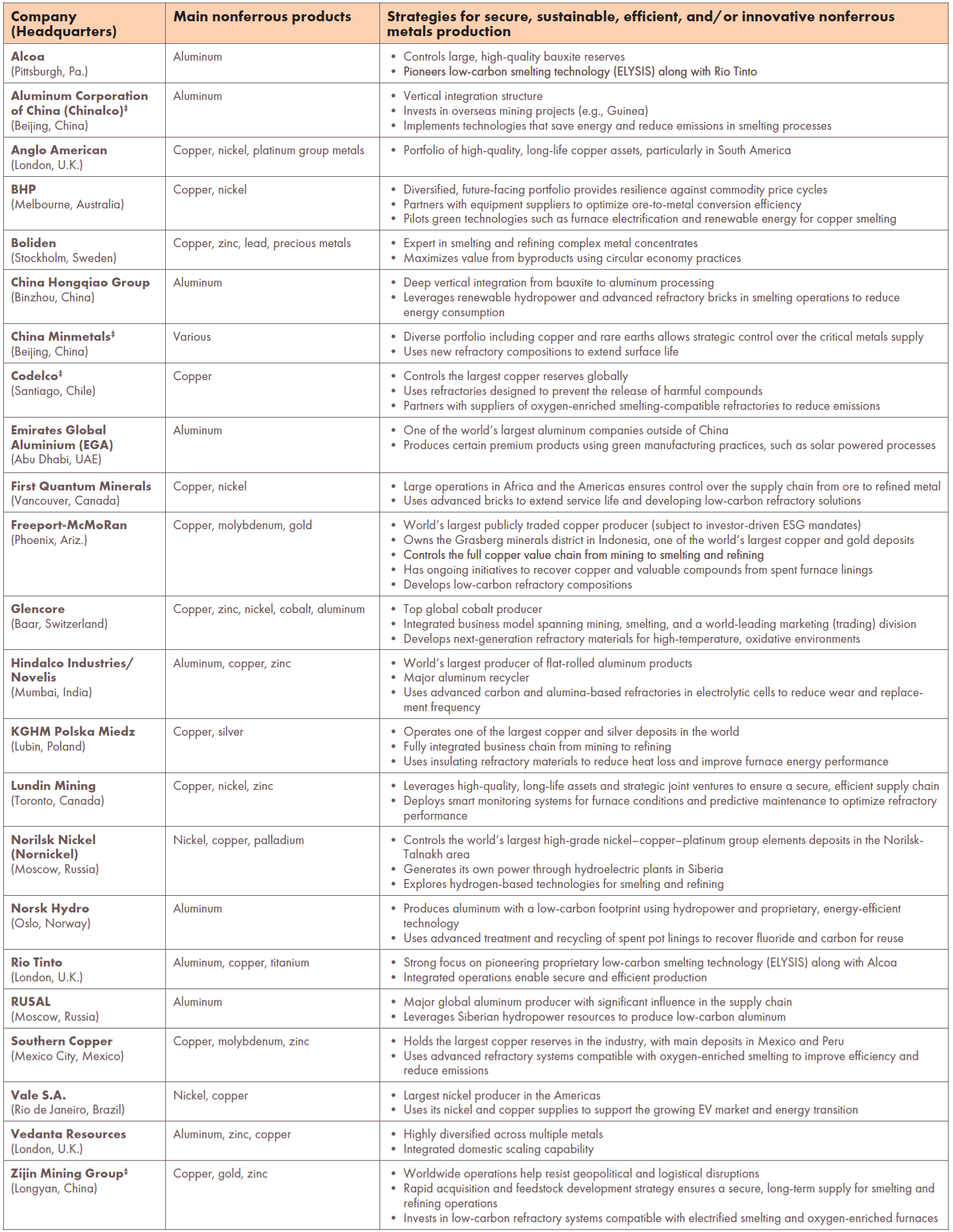

Table 4 highlights companies that are leading the nonferrous metals industry toward a resilient future by developing strategies for stable, cost-effective, and environmentally friendly production. From low-carbon smelting technologies to diversified portfolios, these strategies demonstrate the industry’s commitment to resource security, sustainability, and innovation to meet future market demand.

Table 4. Key players in the nonferrous metals market. Companies marked with ‡ are state-owned enterprises. Source: AMG NewTech

Many of the main innovation pathways being explored currently are in direct response to the challenges detailed in the previous section. For example, environmental and corporate responsibility regulations accelerate the adoption of green smelting, recycling, and artificial intelligence (AI)-driven efficiency,25 which can lower costs over time and open premium markets for low-carbon metals.26,27 Compliance standards are also attracting capital from sustainability-focused funds, improving long-term resilience. Recent industry reports and case studies suggest that companies that adapt early can gain competitive advantages and market share,28 as demand for nonferrous metals remain strong despite regulatory friction.

Current state-of-the art, low-carbon processes, such as hydrometallurgical methods, renewable-sourced electrolytic refining with inert anodes, and emerging direct electrochemical reduction, are very promising in terms of carbon footprint but represent a niche, as they are mainly used for low-grade ores or when very high-purity metals are needed. Consequently, traditional processes remain the primary method for producing nonferrous metals, and improving refractory materials is key to making metal production more efficient and sustainable. The most important refractory-related initiatives are discussed below.

Development of green refractories: These materials have a lower environmental impact because they reduce CO2 emissions during production,29 be that through replacing traditional raw materials with recycled aggregates, industrial byproducts, and alternative binders (e.g., geopolymers) or by using renewable energy to power their fabrication process. The long-term durability and performance of green refractories in the demanding conditions of nonferrous metal production remain an open question, however, one that will shape the future of sustainable metallurgy.

Development of high-performance refractories: Refractories with better resistance to thermal shock and chemical attack are being developed to enhance their durability and lifespan, which correlates with extended furnace life and reduced downtime for maintenance.30 In addition, additive manufacturing allows precise fabrication of refractory products, decreasing material waste and installation time.

Energy-efficient refractory design: The aim is to reduce heat losses and improve furnace insulation to minimize energy consumption. This goal can be achieved by utilizing lightweight insulating refractories for hot-face lining, applying high-emissivity coatings to refractory linings, and employing high-temperature wool as a backup insulation behind dense refractory bricks.31

Development of hydrogen-based metallurgy: Processes utilizing hydrogen plasma for ore reduction are also being developed. These nascent processes provide an impetus for the refractory industry to develop new compositions (e.g., high-corundum or mullite-based materials) because conventional refractory materials can be compromised in the hydrogen environment.32

Digitalization and smart monitoring: Digital transformation is achieved by embedding Internet of Things sensors in the backup layer or near the hot face for real-time monitoring of temperature, heat flux, and wear. AI-driven predictive maintenance is increasingly adopted to extend refractory life, reduce downtime, and optimize energy consumption. AI is also being applied to optimize alloy design, improve smelting efficiency, minimize process waste, and create digital twins. Chinese manufacturers are leading the way in exploring AI in nonferrous metal production. For example, in 2024, Bejiing-based Aluminum Corp. of China established an AI computing center and developed the industry’s first general-purpose large language model, called Kun’an, that is designed specifically to help optimize operational workflows throughout the entire nonferrous metals production process, from exploration and mining to smelting and recycling.33

Recycling and circular economy programs: Spent refractories generate large quantities of waste annually. Recycling programs aim to recover this waste and reuse it to produce new refractories.

Just as refractories are being recycled back into new products, the nonferrous metal industry is also rapidly advancing production of secondary metals, i.e., metals that are recovered from scrap, waste, and used products rather than mined from ore. Tight ore supplies for nonferrous metals such as copper and zinc due to slow mine development are a key reason to accelerate the scale-up of secondary sourcing and reduce reliance on virgin ores.

Another reason to adopt secondary metals in production is because metal recycling leads to significant energy savings. For example, the energy intensity of secondary aluminum is on average 8.3 GJ/t versus 174 GJ/t for primary aluminum, corresponding to a 95% reduction. This significant reduction is possible because unlike primary smelting that requires high-temperature, large-scale furnaces lined with high alumina and magnesia chrome bricks, recycling operations typically use modular furnaces lined with monolithic refractories operating at lower temperatures. Globally, at present, 32% of aluminum and copper produced is recycled metal, with this share continuing to rise.34,35

Besides the economic benefits of secondary metal usage, many companies are focusing on the sustainability aspect by highlighting opportunities and competitive advantages in their annual reports and public statements.

“Climate change is at the heart of everything we do for two reasons. First of all, we have to admit that we have a significant carbon footprint and we have to address that,” states Jakob Sausholm, CEO of Rio Tinto, in a Financial Post article.36 “We also do it because … addressing climate change for the world is about building a whole new energy source. It’s about electrifying society; it’s about building renewable energy. It will require more aluminum, more copper, and more battery materials plus a number of other critical minerals. It’s a huge opportunity for us.”

Securing the future of nonferrous metals

As geopolitical and environmental challenges constrain supply of nonferrous metals, the industry is using these constraints as motivation to develop improved and novel production processes. In particular, advancements in the refractory industry address these challenges in numerous ways. For example, refractories with superior thermal shock resistance and chemical stability can extend furnace life and reduce downtime, while smart refractories with embedded sensors and predictive maintenance enable real-time monitoring of wear and thermal conditions. Furthermore, refractories containing recycled aggregates can reduce reliance on virgin raw materials.

Through these innovations and other developments, the nonferrous metals industry is on a solid path to ensuring it meets the rising demand for these metals while strengthening the resilience of global supply chains.

Metals production: Why refractories are essential

Metallic elements are typically found in nature within stable oxides or sulfides. High temperatures are traditionally required to efficiently separate them as molten metal from slag, which avoids impurity entrapment and makes large-scale production economically viable.

However, these extreme conditions create a harsh environment for the processing equipment. Molten metals and slags are highly corrosive and lead to erosion, while thermal cycling can cause severe mechanical stress. These challenges are where refractory materials come in: They can be engineered to provide heat resistance, chemical stability, and structural integrity, forming the protective lining of furnaces, kilns, electrolytic cells, and other equipment. Without refractories, the high-temperature processes that make modern metal production possible would simply not exist.

While iron and steel production dominates refractory consumption (60% or more), nonferrous metals also account for a significant share of consumption at approximately 30–40% of the total refractories market.a

Approximately 75–85% of nonferrous metals have melting points greater than 500°C. They include most transition metals (e.g., nickel, chromium, titanium), refractory metals (e.g., tungsten, molybdenum, tantalum), and lanthanides and actinides (rare earths and nuclear metals). However, even nonferrous metals with relatively low melting points, such as tin (~230°C), lead (~328°C), and zinc (~420°C), will use refractories for thermal insulation, corrosion resistance, wear resistance, and purity control. Therefore, refractories find application during processing of virtually all nonferrous metals.

References

a“Refractories market size, share, and growth forecast, 2025–2032,” Persistence Market Research. Published October 2025.

Related Articles

Bulletin Features

Emerging Professionals: Science for Society & Future Focus

Science for Society articles: Rishabh Kundu and Ryan C. Eaton: “One small tweak to the lens of materials research, one giant leap for mankind” Grace Dunham: “Microwave firing: Inspiring young scientists through rapid ceramic demos” Hossein Libre: “Shaping materials science through policy engagement” Future Focus articles: Kartik Nemani: “Hope and…

Bulletin Features

Emerging Professionals: Research Articles

Experiential learning: Developing the next generation of engineers By Ryan Eaton When a measure becomes a target, it ceases to be a good measure. Goodhart’s law, coined in reference to monetary policy, is readily applicable to engineering education. When students begin optimizing their study habits to pass an exam rather…

Bulletin Features

Durable and programmable metasurfaces enabled by phase change materials

Controlling light with high spatial precision enables technologies ranging from imaging and sensing to communications. Traditionally, optical components such as lenses and filters rely on bulk materials and fixed geometries, which limit their ability to adapt dynamically. Metasurfaces offer a fundamentally different approach. These materials consist of planar arrays of…