Those who say the refractory industry is old are right. The oldest known furnace was built with sun-dried bricks in Yarim-Tepe, Iraq, around 6000 B.C.1 In a sense, too, the history of the ages—Stone Age, Bronze Age, Iron Age—is a history of refractory technology. Stone Age era civilizations used kilns to fuse and anneal glass, fire brick, smelt ore, and make rudimentary cement and gypsum. Civilizations that discovered the metallurgy that gave name to the Bronze Age and Iron Age gained technological advantages over neighboring civilizations, usually through improved weaponry that allowed them to claim resources.

The Industrial Revolution exploded out of advances in ironmaking technology and steam power. Larger blast furnaces operated at higher temperatures, and invention of the rolling mill expedited metal forming for making machinery for manufacturing.

However, none of these metallurgical advances would be possible without prior seminal advances in furnace building and the refractories within.

Refractories—the “silent partners” of manufacturing—make possible anything made of metal, glass, or ceramic. They are essential to petrochemical and chemical processing.

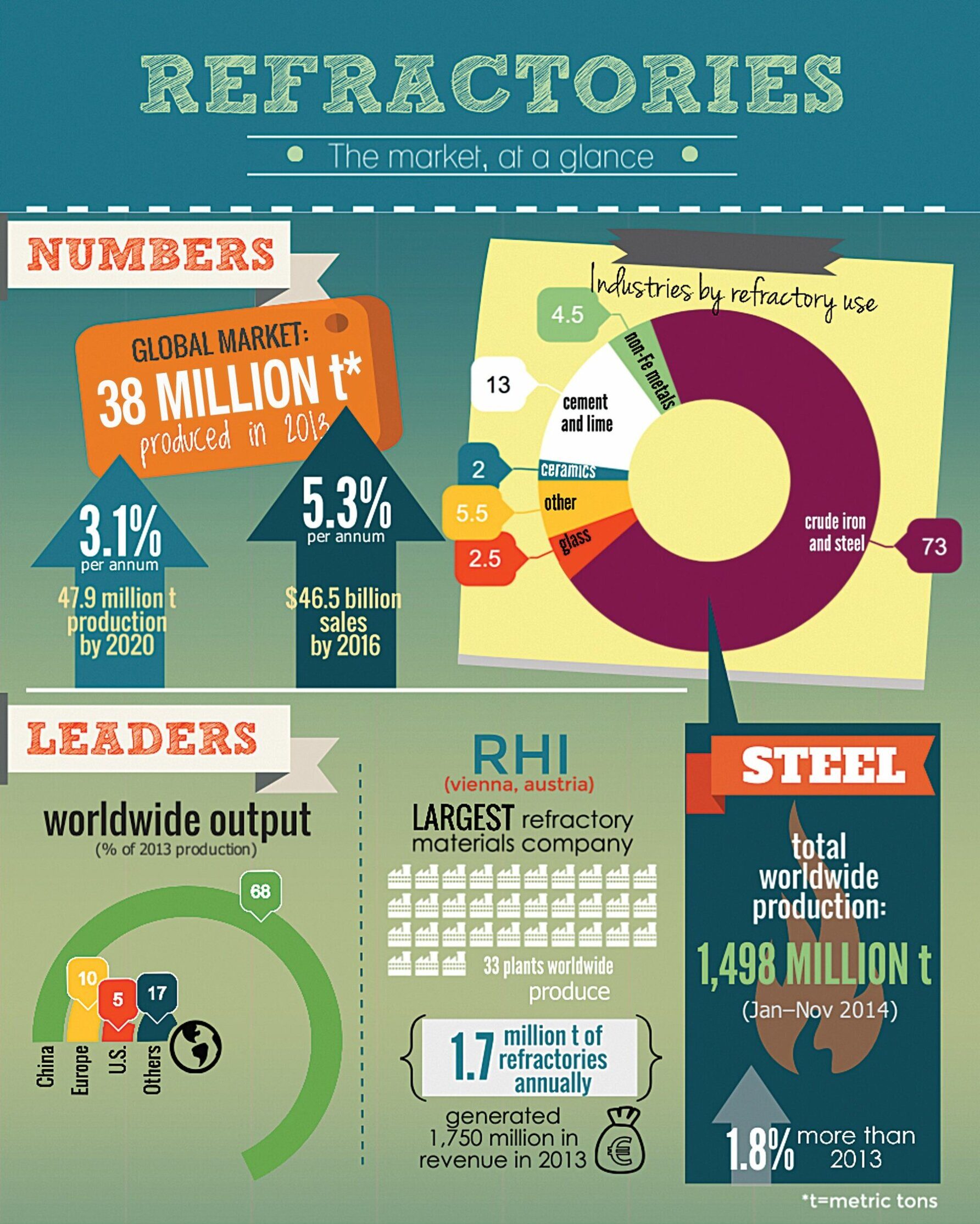

Hidden from view, advances in refractory engineering tend to be known only to those in the field. However, every advance in refractory technology goes straight to the bottom line, especially in the steel industry, which consumes 65%–75% of global refractory production (see infographic, below).

Steelmaking requires a wide range of refractory products, each designed for specific functions. A basic oxygen furnace (BOF), for example, is built with about 10 refractory brick types to achieve uniform wear in the furnace. Other elements of the steelmaking process, such as the tundish, ladle, and continuous caster, call for specialized refractory slide gates, purge plugs, lances, and more.

Material savings translate to cost savings in manufacturing. For example, improved design and installation reduced refractory usage in steelmaking from 60 kg/ton in 1950 to 15 kg/ton in 2014—a 75% reduction in materials.2 Refractory service life affects the bottom line, too. In the decade from 1986 to 1996, LTV-Inland Steel (now defunct and absorbed into ArcelorMittal) in the United States increased BOF converter lining heats from 2,000 to more than 48,000. Baosteel in China and Tata Steel in India also increased BOF lining service lifetimes, although not as dramatically. These advances are critical because unplanned downtime in a steel plant is costly—up to $1,000 per minute.2

In the industries they enable, refractories of the future will be expected to do more than handle heat, optimize energy usage, and minimize environment impact. Controlling nanoscale features of the refractories will improve rigidity, toughness, thermal shock resistance, and corrosion resistance. And incorporating silica nanoparticles into castable refractory formulations will enhance flow, resulting in a denser refractory.3 Future refractories may be bendable and self-healing, or may work to reduce inclusions and other defects in molten metals.2

A recent report presented a refractory research roadmap with a 10-year horizon that addresses materials testing, processing, preparation, and synthesis to advance strategic goals, such as energy and resource efficiency, while balancing economic and material property requirements.4 The roadmap identified key areas for research, including alternative raw materials, refractory recycling, near-net shaping, rapid prototyping, surface engineering, bioinspired materials, and modeling and simulation studies. Advancing refractory technology will require accurate high-temperature property data and high-temperature testing instruments—always a challenge.

As it has for millennia, refractories will continue to serve as “silent partners” to the metal, glass, ceramic, and chemical industries. However, the partners know that this silence is “golden” and speaks to their bottom lines in technical, environmental, safety, and economical terms.

Credit: A. Gocha. Sources: ReportsnReports, “Global and China Refractory Material Industry Report, 2014–2016,” 2014. Jessica Roberts, Roskill Information Services, “Outlook for refractory end markets to 2020,” 2014. Freedonia Group. “Refractories,” 2012. AIST, Iron & Steel Technology, Vol. 12, No. 2, 2015.

Related Articles

Bulletin Features

Emerging Professionals: Science for Society & Future Focus

Science for Society articles: Rishabh Kundu and Ryan C. Eaton: “One small tweak to the lens of materials research, one giant leap for mankind” Grace Dunham: “Microwave firing: Inspiring young scientists through rapid ceramic demos” Hossein Libre: “Shaping materials science through policy engagement” Future Focus articles: Kartik Nemani: “Hope and…

Bulletin Features

Emerging Professionals: Research Articles

Experiential learning: Developing the next generation of engineers By Ryan Eaton When a measure becomes a target, it ceases to be a good measure. Goodhart’s law, coined in reference to monetary policy, is readily applicable to engineering education. When students begin optimizing their study habits to pass an exam rather…

Bulletin Features

Durable and programmable metasurfaces enabled by phase change materials

Controlling light with high spatial precision enables technologies ranging from imaging and sensing to communications. Traditionally, optical components such as lenses and filters rely on bulk materials and fixed geometries, which limit their ability to adapt dynamically. Metasurfaces offer a fundamentally different approach. These materials consist of planar arrays of…